Cyber Fraud Awareness in Banking

In my role as a Cybersecurity Incident Response Analyst at an Indian bank, I routinely handle fraud-related alerts involving customer accounts, social engineering, phishing, malicious applications, and impersonation attempts. Over the past four months, I have observed that most fraud cases follow a similar pattern: attackers exploit trust, urgency, and misinformation to gain access to sensitive credentials or authorize & unauthorized transactions.

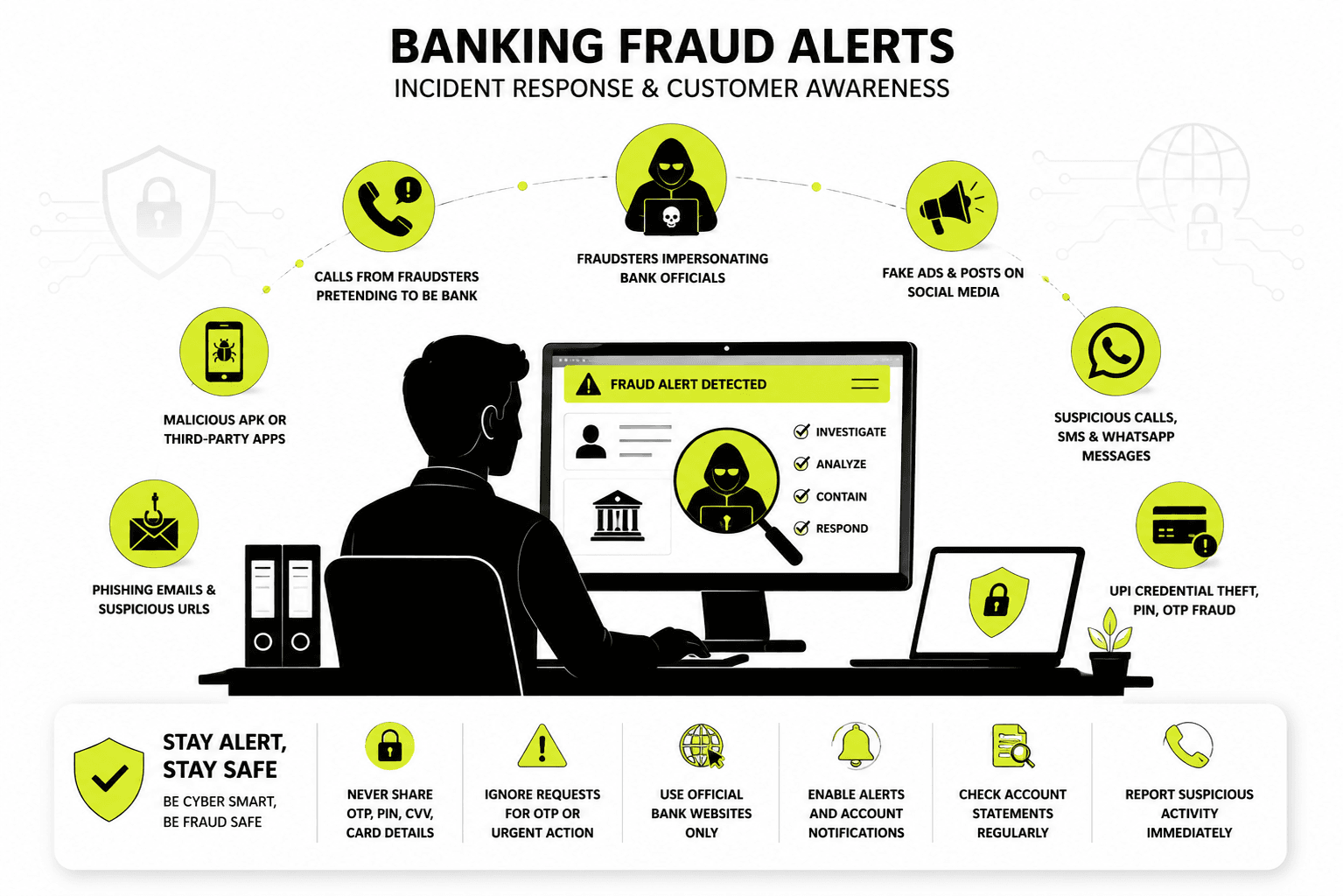

The common fraud indicators I investigate include:

- Installation of APKs or third-party applications outside official app stores

- Calls made by fraudsters impersonating bank representatives

- Fake advertisements or posts on platforms such as Facebook, Instagram, LinkedIn, and Telegram

- Fraudsters impersonating senior bank officials and contacting bank staff

- Clicking on malicious or suspicious URLs received through email

- Calls or messages received from suspicious mobile numbers linked to fraud

- WhatsApp numbers used to share fraudulent instructions or malicious links

- Cases where the customer knowingly shared UPI credentials, PIN, OTP, or approved a transaction under pressure or deception

Initial Response Workflow

When such an alert is received, we first coordinate with the reporting branch manager to collect the required details from the customer. This information helps us identify the fraud channel, understand the attack vector, and determine the correct response. We typically request a brief description of how the incident occurred, based on the customer’s account.

While waiting for branch input, we escalate the reported mail to the internal team responsible for taking immediate action on the suspicious transaction or fraud attempt.

Once the branch manager shares the details, we analyze the case and take action based on the fraud type.

Response Actions by Fraud Type

1. APK or Third-Party Application Fraud

If the customer has installed a suspicious APK or third-party application, we treat it as a potential malware delivery vector. The malicious APK file is forwarded to the Threat Intelligence team for takedown activity. Additionally, we also report the malicious application to the Google Play Store and Apple App Store, along with the relevant platform or social media team through which the application was distributed, such as WhatsApp or Telegram. This helps prevent further distribution of the malicious application and reduces the risk of additional victims.

2. Fraudsters Impersonating the Bank

If the fraudster contacted the customer while pretending to represent the bank, we first determine how the interaction started.

- If it began through a phishing email, we apply the email-based response process.

- If it originated through social media, we follow the social media takedown process.

- We also block the phone number through the relevant threat intelligence workflow.

3. Fake Social Media Advertisements

For fake advertisements or misleading social media posts using the bank’s name, logo, or branding, we extract the malicious URL and send it for takedown. These campaigns are treated as brand impersonation and social engineering attempts. They are especially dangerous because they can mislead customers into sharing sensitive banking information or making fraudulent payments.

4. Fraudsters Impersonating Senior Bank Officials

In cases where fraudsters contact bank staff and pose as senior officials, we verify what information was shared and assess the impact.

- If the activity resulted in a transaction fraud, we involve the internal team responsible for transaction-level response.

- If the fraud involves credit or debit card exposure, we escalate it to the card team for immediate blocking and remediation.

- If user credentials were exposed, we initiate a password reset, request an antivirus scan on the affected machine, and ask the SOC team to monitor the user ID and endpoint for suspicious activity.

This monitoring includes alerts related to:

- Active Directory events

- Phishing emails sent from the compromised account

- Any unusual behavior involving the user ID or endpoint

Monitoring duration depends on the sensitivity of the user’s role and the severity of exposure. We also send the fraud contact number to threat intelligence for blocking. If the impersonation came through social media, we handle it using the social media takedown process.

In parallel, HR is informed to ensure the affected employee is made aware of the incident, understands the associated security risks, and completes the bank’s mandatory security awareness and phishing training course.

5. Malicious or Suspicious URLs Delivered by Email

If the customer clicked on a suspicious URL received in email, we request the original message from the branch manager and analyze it to confirm the threat. Based on the findings:

- If a card is affected, we escalate to the card team for blocking and remediation.

- We request the customer to reset the password associated with the affected email account.

- We recommend enabling multi-factor authentication wherever possible.

- We block malicious email addresses, sender domains, sender IPs, and URLs in the relevant security controls.

- If the compromised mailbox was used to send fraudulent emails, we notify recipients and advise them not to trust those messages.

6. Suspicious Mobile Numbers or WhatsApp Numbers

When the fraud involves a mobile number or WhatsApp number used to send instructions, links, or deceptive messages, we correlate the case with the original source:

- If it is linked to phishing email, we follow the email response process.

- If it is linked to social media, we follow the social media response process.

- We block the number through threat intelligence and related control systems.

7. UPI Credential Disclosure or Transaction Approval Under Pressure

If the customer knowingly entered UPI credentials, PIN, OTP, or approved a transaction under instruction or pressure, we treat it as a high-risk fraud case.

- We coordinate with the debit card team to block the card if required.

- We may block or freeze the account depending on the customer’s response and risk assessment.

- We also instruct the customer to reset the password for the associated email account, following the bank’s password policy.

Awareness and Communication

A key part of the response process is awareness communication. We send security awareness notifications to customers and bank staff to inform them about active fraud trends, phishing campaigns, fake social media advertisements, fraudulent phone numbers, malicious email addresses, and impersonation attempts.

This awareness step is important because fraud campaigns often circulate across multiple channels at the same time. A customer may receive the same malicious content through email, SMS, WhatsApp, or social media, and timely awareness reduces the chance of compromise.

Customer Safety Guidance

At the bank, customer safety is a top priority. Fraudsters use social engineering, impersonation, and deceptive digital content to extract sensitive information such as card details, passwords, PINs, OTPs, and account access credentials.

Customers should follow these core security practices:

- Never share card details, OTPs, CVV, expiry date, or passwords with anyone

- Treat requests for OTPs or urgent action as suspicious

- Use only official bank websites and verify the URL carefully

- Check for HTTPS, but do not rely on it alone as a trust signal

- Enable transaction alerts and account notifications

- Review account statements regularly for unauthorized activity

- Report suspicious calls, emails, messages, URLs, or app installations immediately

If a customer is unsure how or where to report fraud, they should contact the bank’s customer care team, visit the nearest branch, or refer to the official contact details provided in the bank’s email communications.

Closing Note

Bank fraud prevention is not only about blocking a transaction after it occurs. It is about identifying the fraud pattern early, containing the attack surface, coordinating with the right internal teams, and ensuring that customers and staff are informed before similar attacks spread further.

In incident response, every alert is a signal. The faster we validate the source, contain the impact, and communicate the risk, the better we protect customer funds and trust.